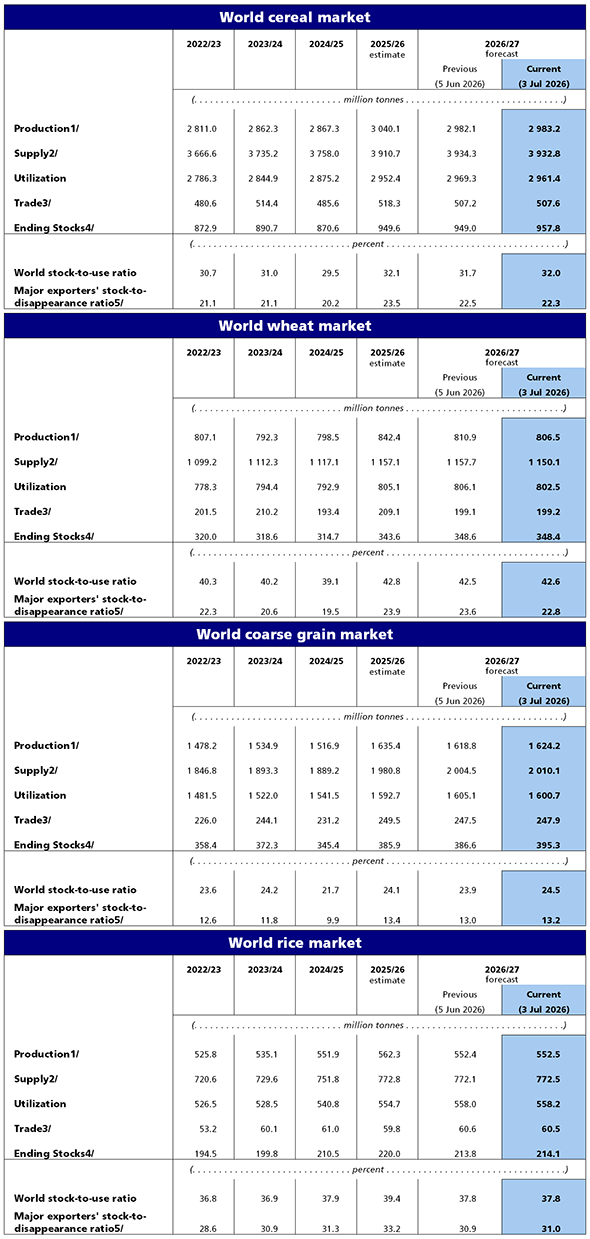

FAO’s latest forecast for global cereal production in 2026 remains broadly unchanged from the previous month, as improved prospects for maize have offset downward revisions to the wheat forecast. Pegged at 2 983 million tonnes, the revised outlook stands 1.9 percent below the all-time high of 2025 but would still rank as the second largest output on record.

The forecast for global coarse grain production is revised marginally upward, now at 1 624 million tonnes, and just short of the previous year’s level. The increase reflects expectations of a larger global maize outturn, with recent official estimates from Argentina, Brazil, China (mainland) and Zambia all pointing to stronger harvests than previously anticipated, amid generally favourable weather conditions that have lifted yields to above-average levels. These gains have more than offset reductions to barley production forecasts in Argentina and the European Union. By contrast, the forecast for global wheat production is lowered by 0.5 percent from last month, now standing at 806.5 million tonnes in 2026, down 4.3 percent year on year. The downward revision mainly reflects recent official data from Australia that reaffirm expectations of a decline in wheat output to a level below the five-year average, as an increased likelihood of El Niño-induced below-average rainfall and elevated input costs are foreseen to curtail both plantings and yields, despite recent rainfall in parts of the country. As for rice, FAO has raised its production forecast for Pakistan since June, following the release of official assessments that point to a higher than previously anticipated 2025/26 harvest in the country. A relaxation of cultivation restrictions due to improved water supplies for irrigation has also raised output prospects for Iraq. However, these revisions are largely offset by downgrades for Colombia and Viet Nam, in both cases owing to lower area sown expectations. As a result, global rice production in 2026/27 is now anticipated in the order of 552.5 million tonnes (milled basis), little changed from June expectations and 1.8 percent below the 2025/26 all-time high.

FAO’s forecast for world cereal utilization in 2026/27 is lowered by 7.9 million tonnes (0.3 percent) this month to 2 961 million tonnes and is now 8.9 million tonnes (0.3 percent) above the 2025/26 level. Despite a 4.5-million-tonne cut since the previous forecast in June, utilization of coarse grains is still expected to grow by 8.0 million tonnes (0.5 percent) in 2026/27 driven by higher feed use, especially in South America, and increases in food consumption, mainly in Africa. Global wheat utilization has been reduced by 3.6 million tonnes to 802.5 million tonnes, slightly below the 2025/26 level, largely reflecting lower feed use in China as wheat becomes less competitive with stabilizing maize prices. World rice utilization is forecast to expand by 0.9 percent in 2026/27 to a fresh peak of 558.2 million tonnes, underpinned by a population-driven increase in food use.

At 957.8 million tonnes, FAO’s forecast of world cereal stocks at the close of seasons in 2027 is raised by 8.8 million tonnes from the previous month, pointing to an annual increase of 8.2 million tonnes (0.9 percent). Upward revisions to stocks of wheat and coarse grains more than offset a reduction in rice, leaving the global cereal stock-to-use ratio largely unchanged in 2027 at 32.0 percent. The forecast for global coarse grain inventories is raised by 8.7 million tonnes from the previous report and stocks are now projected to rise by 9.3 million tonnes (2.4 percent) from their opening levels, driven by larger reserves of maize and barley. Maize stocks are expected to expand in China as official estimates foresee another record harvest in 2026 while modest gains are also anticipated in exporting countries such as Argentina, Brazil and Paraguay amid improved production prospects. In contrast, the United States of America is expected to draw down part of its historically high reserves in 2026/27. Barley inventories are also seen rising, now projected to reach 34.3 million tonnes at the end of seasons in 2026/27, following a 3.2-million tonnes upward revision, largely reflecting continued accumulation in China. The forecast for global wheat inventories at the end of seasons in 2026/27 remains almost unchanged this month. However, the year-on-year increase is now expected to be more pronounced as wheat trade picks up in the final stages of the 2025/26 marketing year, reducing carry-in stocks in key exporters such as Argentina, Australia and the European Union, resulting in global wheat stocks growing by 4.8 million tonnes (1.4 percent) from opening levels. Following a minor upward adjustment since June, world rice stocks at the close of 2026/27 marketing seasons are forecast at 214.1 million tonnes, down 2.7 percent from their record opening levels, but still the second highest reserve on record. Rice exporting countries are forecast to account for this reduction, while carry-overs in rice importing countries remain, on aggregate, close to the seven-year highs they reached in 2025/26.

FAO’s forecast for world trade in cereals in 2026/27 is little changed from June at 507.6 million tonnes. However, brisk trade activity towards the end of the 2025/26 marketing year has led to an upward revision for trade in wheat, maize and barley. Consequently, the year-on-year decline in global wheat trade in 2026/27 is now expected to widen to 9.8 million tonnes (4.7 percent) as strong sales performance by Argentina and the European Union lift the 2025/26 global estimate by 3.2 million tonnes to 209.0 million tonnes. Similarly, the contraction in barley trade in 2026/27 is now expected to reach 7.0 million tonnes (18.8 percent) reflecting higher 2025/26 estimates on sustained shipments from Australia, Canada and the European Union, outweighing a slowdown from Ukraine late in the season. Estimates for global maize trade in 2025/26 are also revised upward by 3.0 million tonnes as Argentina and the United States of America maintain market share, despite weaker dispatches from Serbia and Ukraine. Consequently, global maize trade is still expected expand in 2026/27 but now by a lesser margin than previously envisaged, increasing by 5.0 million tonnes (2.5 percent) from the previous season. International rice trade in 2026 (January-December) remains forecast to fall 2.1 percent below the 2025 high to 59.8 million tonnes. Lower imports by Asian countries are expected to drive this slight reduction, although import demand could also ease in all other regions, except for Latin America and the Caribbean, Europe, and Oceania.

Summary Tables

© Association of producers,

Processors and Exporters of Grain, 1997-2026.

When quoting and using any materials

reference to the Ukrainian Grain Association is obligatory.

If you use the Internet, you must also use

the hyperlink to https://uga.ua

![]() Site development

Site development

To register on the website, please contact the administration UGA admin@uga.ua