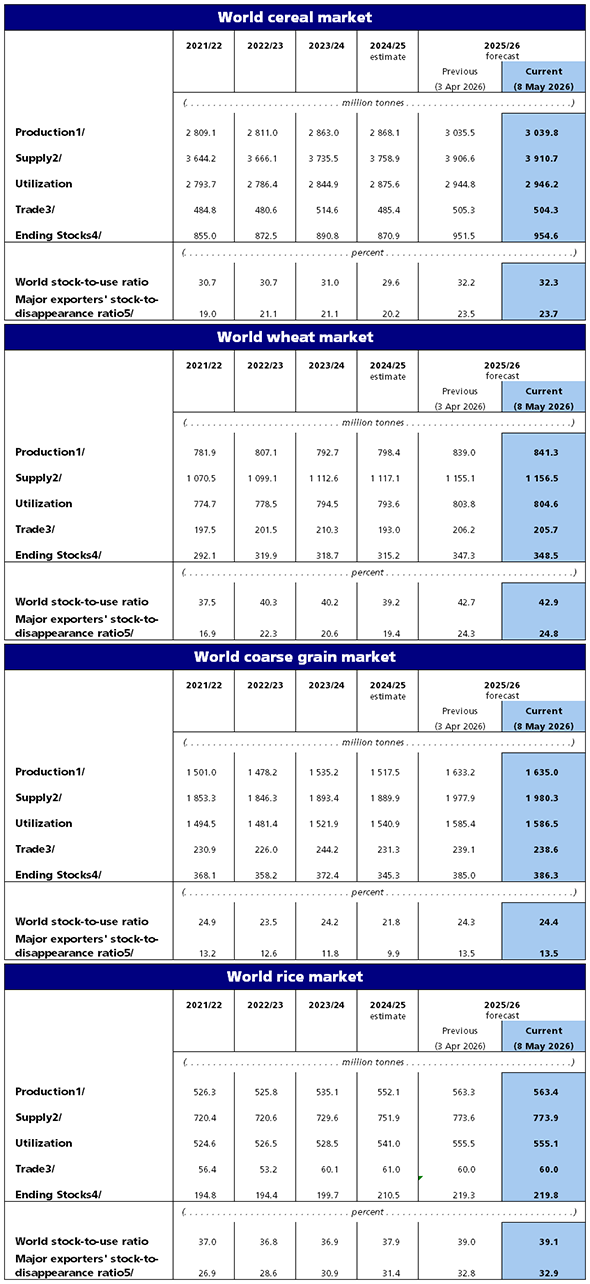

FAO has raised its latest 2025 production forecast for most major cereals this month, further strengthening indications of a generally favourable supply situation in 2025/26. Global cereal production is now pegged at 3 040 million tonnes, representing an increase of 6.0 percent compared to the previous year. Wheat and maize production estimates are lifted by approximately 2 million tonnes each this month, mainly reflecting upward revisions in Europe. Global rice production is forecast to expand by 2.0 percent in 2025/26 to an all-time high of 563.4 million tonnes (milled basis). This level would stand slightly above April expectations, largely due to more buoyant production results reported by officials in Cambodia (namely for the main-crop harvest), Cote d’Ivoire, and Mali.

At 2 946 million tonnes, world cereal utilization in the 2025/26 season is expected to grow by 70.6 million tonnes (2.5 percent) from the previous season with increased usage of all the major cereals, especially maize, rice and wheat. A rise of 33.3 million tonnes (4.5 percent) in the use of maize for animal feed is the biggest single element of the expansion in utilization as large harvests have made both domestic and exportable supplies available at attractive prices. Overall global wheat use is raised marginally this month. While food use of wheat is revised downward following historical revisions made to the Islamic Republic of Iran, Mexico and Türkiye, this decline is more than offset by upward revisions to feed use and other use of wheat in the same countries. Despite a 0.4-million-tonne trimming since April, world rice utilization in 2025/26 remains forecast to expand by a robust 2.6 percent to reach an all-time high of 555.1 million tonnes, reflecting expectations of continued strong growth in food and non-food industrial uses of rice.

FAO’s forecast for world cereal stocks by the close of seasons in 2026 stands at 954.6 million tonnes, pointing to an increase of 9.6 percent above opening levels and indicating record global inventories for wheat and rice. The forecast for global cereal stocks is raised by just 3.1 million tonnes from last month, with a downward revision to the Islamic Republic of Iran more than offset by an upward revision to the Russian Federation, the latter on the latest reports of a better-than-expected wheat harvest in 2025. Stocks of coarse grains are also revised upward this month by 1.4 million tonnes, mainly reflecting higher estimates of reserves of barley, maize and oats, notably in Belarus. Based on this month’s forecasts for stocks and utilization, the global cereal stocks-to-use ratio is forecast to rise from 29.6 percent in the 2024/25 season to 32.3 percent, indicating a comfortable supply level. Since April, FAO has raised its forecast of world rice stocks by 0.6 million tonnes, chiefly due to upgrades to anticipated reserves in Cambodia, consistent with the improved supply outlook for the country, and in Japan and the United States of America, owing to more subdued demand prospects. As a result, global rice stocks at the close of 2025/26 marketing years are now seen reaching a peak of 219.8 million tonnes, up 4.4 percent year-over-year and sufficient to cover 4.7 months of projected global rice utilization.

World trade in cereals in 2025/25 (July/June) is forecast at 504.3 million tonnes, representing an expansion of 18.9 million tonnes (3.9 percent) from the 2024/25 level. Despite disruptions affecting global trade across commodities, trade in cereals has maintained its expected pace during the first months of 2026. Minor downward revisions are made this month to trade in wheat and maize based on the latest import information for, respectively, Ethiopia and the United Kingdom of Great Britain and Northern Ireland. International rice trade is forecast at 60.0 million tonnes in 2026 (January-December), essentially unchanged from April expectations. Although at that level world rice flows would stand 1.6 percent below the 2025 peak, they would still represent the second largest trade volume on record, mirroring prospects of continued growth in purchases by countries located in Africa and Europe, as well as a recovery in imports by Latin America and the Caribbean.

Although conditions remain broadly favourable in most regions, wheat and maize production outlook for 2026 under rising input cost pressures

For 2026 crops, FAO’s latest forecast for world wheat production has been trimmed marginally this month, now standing at 817 million tonnes. This represents a decline of about 2 percent year on year, although the expected output remains above the previous five-year average. The outlook continues to face some uncertainty, amid the effective closure of the Strait of Hormuz that drove up input costs, notably energy and fertilizers, alongside relatively softer wheat prices. These factors are compressing farmers’ margins and could negatively affect wheat planting decisions, as well as reduce fertilizer application rates, with potential implications for yields. Similar cost-price dynamics are also influencing the production outlook for 2026 maize crops, with the added caveat of heightened demand for maize-based biofuel in response to elevated crude oil prices.

Across much of the European Union, continued favourable weather conditions have maintained stable wheat yield prospects, although emerging rainfall deficits in central and eastern parts have raised some concerns. Overall, wheat production is foreseen to decline year on year, driven by a price-driven reduction in sowings and expectations of yields returning to average levels after the highs of 2025. Winter wheat crop conditions in the United Kingdom of Great Britain and Northern Ireland are reportedly more favourable this year compared to last, and production is expected to increase moderately in 2026. In the Russian Federation, harvest expectations remain broadly unchanged this month, with lower plantings continuing to underpin prospects of a smaller outturn in 2026. In Ukraine, the wheat production forecast remains unchanged and at a comparable level to the previous year – albeit still well below pre-conflict levels – as improved yield prospects under favourable weather conditions are expected to offset reductions in the harvested area. In the United States of America, a contraction in the area planted mainly underlies expectations of a lower wheat harvest in 2026, while expanding drought conditions, reflected in poorer crop conditions in April 2026 compared to the previous year, are weighing on wheat yield prospects; these developments prompt a modest downward revision to the production forecast this month. The wheat production forecast for Canada remains unchanged, with expectations still pointing to a year-on-year decline, reflecting earlier indications of a contraction in plantings and an anticipated drop in yields to near-average levels. In India, despite some recent localised weather irregularities, the outlook continues to point to a record wheat harvest, largely underpinned by historically high sowings. Production forecasts for Pakistan and China (mainland) are kept unchanged in April, and both countries are expected to harvest above-average wheat crops. In Near East Asia, continued favourable weather conditions are bolstering yield prospects in Türkiye, contributing to an upward adjustment of the production forecast this month and reinforcing the above-average harvest expectations in 2026. Similarly beneficial weather conditions are also supporting crop prospects in the Islamic Republic of Iran. In North Africa, after a slow start to the season, ample precipitation since December has pushed up vegetation indexes to above-average levels, suggesting production rebounds in 2026 after two consecutive years of drought-affected harvests. In southern hemisphere countries, planting of the main season wheat crop is underway. In Australia, the 2026 production forecast has been trimmed relative to the preliminary outlook, reflecting a higher likelihood of below-average rainfall associated with a potential El Niño event that is likely to constrain yields, coupled with elevated input costs. Similar concerns are evident in South Africa, where early indications point to a reduction in wheat sowings to below the five-year average, driven by unfavourable weather expectations and tighter farmer margins.

Regarding the 2026 maize crops, harvesting is already underway in southern hemisphere countries, while planting has commenced in northern hemisphere countries. In Brazil, maize production is expected to remain above average in 2026, supported by favourable weather conditions and a slight increase in plantings encouraged by robust export demand. In Argentina, higher-than-expected sowings combined with improved rainfall conditions are supporting above-average yield prospects, raising the possibility that maize production could reach record levels in 2026. In South Africa, continued favourable growing conditions are underpinning expectations of above-average yields; together with a modest increase in the planted area, total maize production could approach the record level of about 17.5 million tonnes last observed in 2017.

© Association of producers,

Processors and Exporters of Grain, 1997-2026.

When quoting and using any materials

reference to the Ukrainian Grain Association is obligatory.

If you use the Internet, you must also use

the hyperlink to https://uga.ua

![]() Site development

Site development

To register on the website, please contact the administration UGA admin@uga.ua